February 24, 2025 | 3.5 Minute Read

Selling a rental portfolio is a major financial decision that requires careful analysis. Whether an investor is looking to cash out, diversify assets, or simplify management, understanding the numbers and potential pitfalls for a buyer is essential.

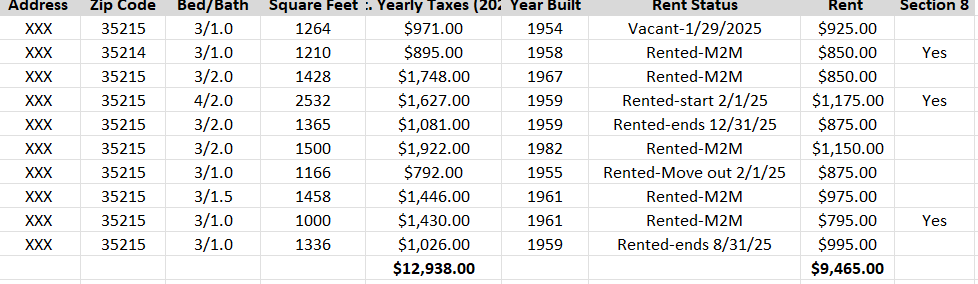

Recently, I reviewed an off-market portfolio of 10 rental properties in Birmingham, presented by an agent. The portfolio generates $9,465 in monthly rent, with an asking price of $1.1 million.

Here’s the list (Addresses removed).

Do you see the red flags? Let’s break it down.

Price Per Door

The $1.1 million asking price equates to $110,000 per property. While this may be reasonable for homes rented at $1,100 or more per month, it is much less attractive for properties renting less than $1,000. Paying the same price per door across the portfolio without considering individual rent levels raises concerns. Often sellers package properties together to offload underperforming or undesirable assets at the same price per door. Usually, this is discovered during inspection and due diligence and often buyers will want to renegotiate as a result.Lease Structure

Five of the ten leases are month-to-month. This offers flexibility if rents are below market (which most are with this portfolio), allowing for tenant turnover and potential rent increases. However, turnover means potential vacancy and repair costs, which could erode cash flow. If keeping the tenants is the plan, securing new annual leases would be recommended prior to closing.

One property is vacant. Its condition and whether the seller plans to lease it before closing are crucial factors that will impact overall cash flow. It may be a distressed asset that requires renovations to become rent-ready. Will the seller lease it out before closing, or will it be the buyer’s responsibility after purchase?

1% Rule

Many investors use the 1% rule, which suggests that a rental property should generate at least 1% of its purchase price in monthly rent. In this case, the target would be $10,100 per month. With current rents totaling $9,465, the portfolio falls about 6% short of this metric, which can significantly affect returns. Would the buyer turnover tenants to raise the rents to meet this baseline and incur vacancy and renovation costs or accept the current cash flow?Financing

If financing with a Debt Service Coverage Ratio (DSCR) loan, let’s assume:Purchase Price: $1.1M

Taxes: $12,938 annually

Insurance: $12,500 annually

Loan Terms: 80% LTV at 7.5% interest

This results is a net monthly cash flow of $1,192.08 with a 1.19 DSCR—barely meeting lender requirements. Most lenders require a minimum 1.2 DSCR, meaning either the loan amount would need to be reduced to 79.5% LTV, or the seller would need to lower the price by at least $5,500 to make raise the DSCR to 1.2. Would you invest $1.1M for a 0.001% cash flow return based on the current price?

Operational Costs

But wait! We haven’t accounted for property management (10%), vacancy rate (5%), and maintenance costs (5%). Unless you plan to manage these properties yourself, you’re now operating at a negative cash flow.

What is the seller thinking?

Expecting a Cash Buyer

The seller may assume an all-cash buyer who evaluates cash flow differently. If no financing is involved:Gross Rent: $9,465

Taxes & Insurance: $2,488

Estimated Management & Cap Ex (20% Deduction): $1,895

Net Monthly Income: $5,582, or $66,979 annually

While this might seem like strong cash flow, most investors will leverage financing, which outlines above becomes negative cash flow.

Relying on Comparable Sales

The seller appears to be pricing the portfolio based on comparable properties valued at $110,000 per door. However, he is not accounting for the fact that lower rents reduce financing viability. Let’s run the numbers on the one property currently renting at $795 per month:After taxes, insurance, and 20% management/cap ex deductions, the monthly cash flow is $436.

If financed with an 80% loan at 7.5%, the property would lose $28.64 per month before even factoring in reserves and a very poor 0.94 DSCR which would not qualify for a loan.

While bundling the portfolio into a single loan may help offset weaker-performing properties, 8 out of 10 units would struggle to qualify for financing individually at current rent levels. Acceptable as a portfolio loan but what if you want to finance them individually at the current rents?

Portfolio Must Be Sold Intact

The seller claims that the lender will not allow individual properties to be sold separately. However, most portfolio lenders will permit a sale of a property as long as the loan maintains an acceptable loan-to-value (LTV) ratio. Typically, lenders will allow an individual sale at 115%-120% of the market value of the single property, meaning the seller wouldn’t necessarily lose money—he would simply retain more equity in the remaining properties and have it tied up in the current loan. This is most likely something the seller wants to avoid.Additionally, most lenders do not allow loan recasting. Even though the mortgage balance is now lower, the monthly payment amount remains the same. The borrower is effectively paying down their debt faster. This is a crucial consideration for investors looking to sell properties financed through portfolio loans. Most investors are not aware of this until they try and sell individual properties from a portfolio loan.

While this portfolio may seem attractive at first glance, a closer examination reveals challenges related to pricing, lease structures, financing, and individual property performance. The numbers simply don’t work well for a financed buyer unless rents can be increased, terms adjusted, or the purchase price negotiated down.

For investors considering such deals, it’s critical to analyze cash flow, lease terms, financing options, and property conditions before making a decision. The seller may see strong cash flow potential, but most experienced buyers—especially those leveraging debt—will see a property with no cash flow. Either the buyer will need to negotiate a much lower price or walk away.