January 13, 2025 | 2.5 Minute Read

Before the crash of 2008, I was doing very well flipping houses in the Miami/Fort Lauderdale market. When the warning signs appeared in 2006, I ignored them and took on unnecessary risk and it costs me dearly.

It was only after the crash that I learned some hard fought lessons and vowed to never put myself in that position again.

In 2015, I started acquiring rental properties in Birmingham, AL taking advantage of lower home prices. By 2020, I had grown my portfolio to over 85 rental properties. I’ve sold off several turnkey properties as was the strategy back then and now own 55 door currently.

So, how do I see the market in 2025? I compare it to the housing market of the early 1980s, a period marked by rapidly rising interest rates and strained affordability. My opinion was reinforced beginning in 2022 after Federal Reserve Chair Jerome Powell signaled impending economic challenges. The result has been a significant drop in housing transactions, echoing patterns from 1978 to 1981 when existing home sales fell by 50% while median home prices continued to rise.

The current housing market is fundamentally broken due to the disappearance of “move-up buyers.” Traditionally, these buyers would sell their starter homes and purchase larger ones, driving two transactions in the market. However, homeowners who purchased properties in 2020 or 2021 at low-interest rates now face a dilemma: moving up would mean significantly higher home prices and mortgage rates, making the math untenable. This stagnation in entry-level housing creates a ripple effect, limiting overall market activity and skewing median home price data.

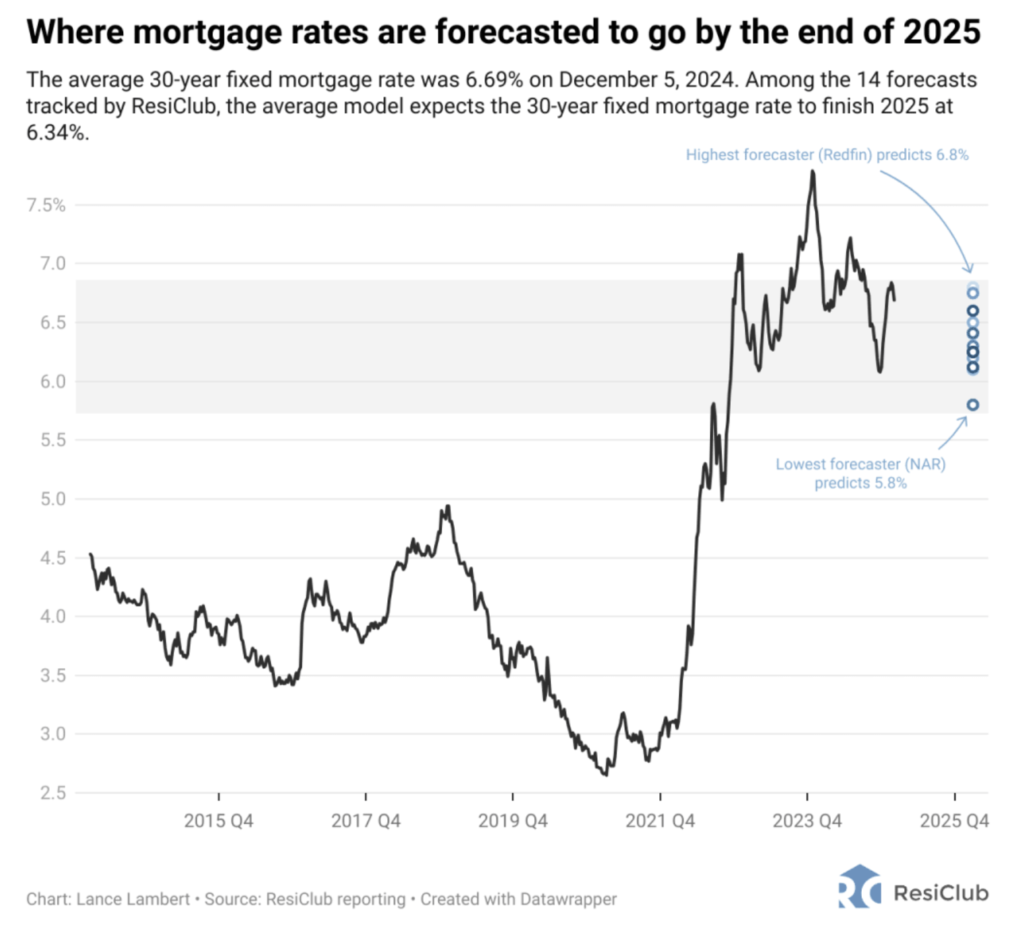

Looking ahead to 2025, I predict a continuation of the “higher for longer” interest rate environment, with rates likely averaging around 7%. I expect housing transaction volumes to remain low, with national home prices staying relatively flat, increasing by 1% to 2%. Builders may shift focus to smaller, entry-level homes to meet demand. However, I do not not foresee new first-time homebuyer programs that would increase demand, as supply remains the primary issue.

There you have it—my predictions for 2025. We’ll have to wait and see how the year unfolds, and then revisit this in December to see if my forecasts were on target.

Next week, we’ll look at why starter homes in the United States are disappearing.