Skip to content

Skip to content March 25, 2025 | 3 Minute Read

Investing in rental properties with Section 8 tenants can provide stable, government-backed income. Many landlords are drawn to the promise of guaranteed rent payments—especially when the tenant’s voucher covers 100% of the rent. But here’s the truth: just because rent is guaranteed doesn’t mean every Section 8 applicant should be approved.

Section 8 is a rental assistance program, not a tenant approval system. Landlords are still responsible for screening applicants thoroughly. While the government may pay the rent, that doesn’t mean the tenant will be a good fit or take care of your property. That’s why every Section 8 applicant we consider goes through the same screening process as any other tenant.

How We Market Our Rentals

We list our properties on AffordableHousing.com and Zillow, using our CRM system to syndicate listings. Most prospects come through these platforms. Once someone expresses interest, I text them a YouTube video of the property. This helps refresh their memory, especially if they’ve seen multiple properties.

Initial Screening Questions

From the very first call or message, I ask these six questions:

Which housing authority issued your voucher? (We work with three locally.)

Is your rent fully covered by Section 8? If not, how much is your portion?

Why are you moving? (Most say due to poor maintenance at their current rental.)

What is your moving timeline? (Many say “immediately,” but Section 8 typically takes 30 days for approval, inspection, and lease signing.)

How many people will live in the unit? (For example, 2–4 in a 3-bedroom is reasonable. One applicant said 7–8. That is a hard no.)

Do you have any prior evictions or bankruptcies? (We do not want tenants who know how to avoid paying rent)

Showing the Property

We always meet prospective tenants in person. This gives us a chance to assess their behavior and communication style. During the showing, I explain:

Who is responsible for utilities and yard maintenance

Our application and approval process

Red flags like late arrival, poor hygiene (the smell of weed on them) can outweigh a fully covered voucher.

Application Requirements

We require:

Minimum FICO score of 550

No prior evictions or bankruptcies

Even with 100% voucher coverage, poor credit can be a warning sign. Tenants with a history of not paying bills may still cause problems—especially if their voucher later changes to a partial payment.

Why Some Fully Vouchered Applicants Are Rejected

Here’s why some Section 8 applicants are declined, even when the government pays all or most of the rent:

Dishonesty about their credit. If an applicant claims clean credit but we find evictions or criminal records, they’re automatically rejected. Some list a friend or family member as their landlord and with further due diligence, we always find out.

Vouchers can change. Tenants with 100% coverage may be switched to partial vouchers after their annual income review. If their credit is poor, they may struggle to pay their share later—especially after major expenses like buying gifts over the holidays. Paying rent is the last priority.

Income verification. If the tenant pays any portion of the rent, we require they earn 3 times that amount monthly. For example, if they pay $250 partial rent, they must earn $750+ per month. We verify this with two recent pay stubs and employer confirmation. If they don’t qualify, they’re declined.

Debt load matters. Even with full voucher coverage, tenants with large amounts of debt and low credit scores are risky if they later owe any portion of rent. High debt signals poor financial responsibility. I have seen some if these applicants carry debt of over $100,000 in credit cards, car payments, and education costs. Most they simply are not paying on time.

Landlord references. We always speak to their current landlord to confirm they are a tenant in good standing. We research to make sure the person we are actually calling is the landlord and not a family member posing as one. Checking the county records, skip tracing the landlord name, or researching the property management company to make sure this person works there are ways to ensure we are contacting the right person.

Recent Rejections:

1. Partial voucher, unstable household:

A tenant with a $1,247 rent had a partial voucher: Section 8 paid $665, she paid $582. Credit was acceptable, but her income came from unverified cash payments for hairstyling. Her boyfriend, who had verifiable income and was added to the lease, backed out a week before move-in due to a fight with her. He changed his mind the next day, but we cancelled the lease. He is not someone that would not honor a signed lease and we fully expect him to bolt from the property at some point. We don’t do drama and these tenants would have caused us problems had they moved in. Section 8 supported our decision to cancel.

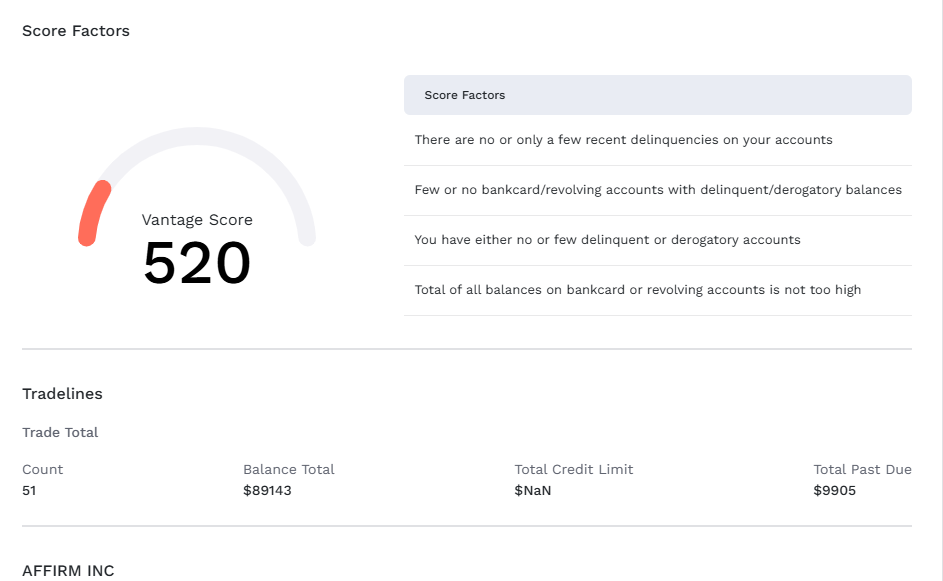

2. 100% voucher, poor credit and high debt:

Another applicant had a 520 credit score and over $89,000 in debt. While Section 8 would initially pay the full rent, any future reduction in coverage would put this tenant at high risk for non-payment. From her credit history, it was clear she was obtaining credit cards but not paying the monthly balances using them as an ATM. She was denied.

Consistent Screening = Peace of Mind

A Section 8 voucher is attractive, but we know that the quality of the tenant matters just as much as the reliability of the rent. Screening Section 8 applicants means evaluating everything from background to communication style—not just whether the government will pay on time.

Section 8 or not, the same rules apply. That’s how we protect our investments, our cash flow, and our peace of mind.