June 22, 2026 | 3 Minute Read

The average home in the United States is now selling for less than its list price, and new data from Realtor.com shows how quickly sellers lose negotiating power when a property sits on the market.

The first month is the most important period in a listing’s lifecycle. Sellers who price correctly and generate early interest are seeing the strongest results, while those who miss the mark often face increasing pressure to reduce their price.

Here are the key findings:

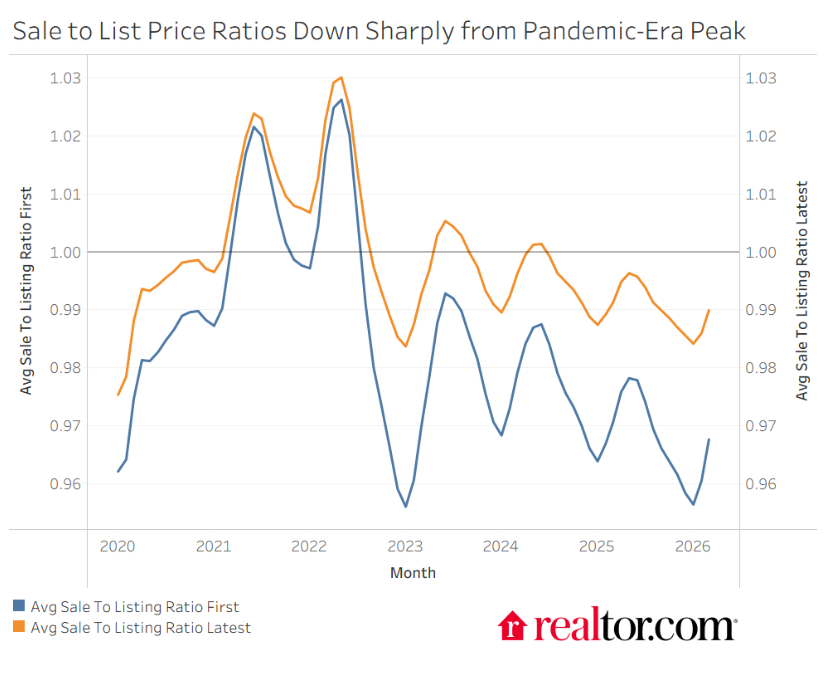

- Homes are selling below asking price. The national sale-to-list price ratio has fallen below 1.0, meaning the typical home is now closing for less than its original asking price. This is a significant change from the pandemic housing boom, when bidding wars routinely pushed prices above list price.

- The first four weeks matter most. Homes that sold around the four-week mark achieved the best results, closing an average of 1.8 percentage points above the monthly average. The strongest-performing listings typically went under contract within the first two weeks.

- Longer market time leads to lower sale prices. Homes that remained on the market for 18 weeks sold an average of 1.3 percentage points below the monthly average. The gap between the best and worst timing outcomes exceeds 3 percentage points.

- Price reductions are happening later. During the peak of the seller’s market in 2021, price reductions typically peaked around week three. In 2026, that peak has shifted to week six, giving sellers a slightly longer opportunity to attract buyers before price adjustments become necessary.

- Property type and location matter. Condominiums remain the weakest-performing segment, selling for an average of 97.9% of list price compared to 99.2% for single-family homes. Regionally, the Northeast is the only area where the average home still sells above asking price. The South and West continue to favor buyers, with many Sun Belt markets carrying more inventory than they did before the pandemic.

- The move-up market has softened considerably. Homes priced between $750,000 and $2 million generated some of the strongest bidding activity in 2022. Today, that segment has become one of the weakest, with final sale prices falling further below asking price than many other price ranges.

.

For real estate investors, this trend creates both opportunities and risks.

On the acquisition side, a slower market gives investors more negotiating leverage. As homes sit longer, motivated sellers become more willing to reduce prices, offer concessions, or accept creative terms. Investors targeting direct-to-seller deals, fix-and-flips, BRRRR projects, or rental acquisitions may find better buying opportunities than they have seen in several years.

However, investors planning to resell properties need to adjust their expectations. The days of listing a property above market value and expecting multiple offers are largely over in many markets. Profit margins are becoming increasingly dependent on buying right, controlling renovation costs, and pricing accurately from the start.

The data reinforces a lesson many experienced investors already know: the market rewards properties that are priced correctly on day one. A flip that sits on the market for months doesn’t just face a lower sale price—it also accumulates additional holding costs, financing expenses, taxes, insurance, and maintenance costs that eat into profits.

This is especially important in the Sun Belt, where inventory has risen significantly and buyers have more choices. Investors operating in these markets should be particularly conservative when projecting after-repair values (ARVs) and resale timelines. Deals that looked profitable based on 2021 or 2022 assumptions may no longer work in today’s environment.

The biggest winners over the next 12 to 24 months are likely to be investors who maintain strict underwriting standards, negotiate aggressively on acquisitions, and avoid relying on future appreciation to make a deal work. As leverage shifts from sellers to buyers, investors who have patience and capital will have more opportunities to purchase quality assets at favorable prices.

In short, this market is becoming less forgiving for investors who overpay and more rewarding for those who buy with discipline.